STATE OF CAPTURE

Report on an investigation into alleged improper and unethical conduct by the President and other state functionaries relating to alleged improper relationships and involvement of the Gupta family in the removal and appointment of Ministers and Directors of State-Owned Enterprises resulting in improper and possibly corrupt award of state contracts and benefits to the Gupta family's businesses

Report No: 6 of 2016/17

“One of the crucial elements of our constitutional vision is to make a decisive break from the unchecked abuse of State power and resources that was virtually institutionalised during the apartheid era. To achieve this goal‚ we adopted accountability‚ the rule of law and the supremacy of the Constitution as values of our constitutional democracy. For this reason‚ public office- bearers ignore their constitutional obligations at their peril. This is so because constitutionalism‚ accountability and the rule of law constitute the sharp and mighty sword that stands ready to chop the ugly head of impunity off its stiffened neck.

It is against this backdrop that the following remarks must be understood:

“Certain values in the Constitution have been designated as foundational to our democracy. This in turn means that as pillar-stones of this democracy‚ they must be observed scrupulously. If these values are not observed and their precepts not carried out conscientiously‚ we have a recipe for a constitutional crisis of great magnitude. In a State predicated on a desire to maintain the rule of law‚ it is imperative that one and all should be driven by a moral obligation to ensure the continued survival of our democracy.” And the role of these foundational values in helping to strengthen and sustain our constitutional democracy sits at the heart of this application.”

Economic Freedom Fighters v Speaker of the National Assembly and Others; Democratic Alliance v Speaker of the National Assembly and Others [2016] ZACC 11

Executive Summary

(i) “State of Capture” is my report in terms of section 182(1)(b) of the Constitution of the Republic of South Africa, 1996, and section 3(1) of the Executive Members Ethics Act and section 8(1) of the Public Protector Act, 1994.

(ii) This report relates to an investigation into complaints of alleged improper and unethical conduct by the president and other state functionaries relating to alleged improper relationships and involvement of the Gupta family in the removal and appointment of ministers and directors of State Owned Entities (SOEs) resulting in improper and possibly corrupt award of state contracts and benefits to the Gupta family’s businesses.

(iii) The Public Protector received three complaints in connection with the alleged improper and unethical conduct relating to the appointments of Cabinet Ministers, Directors and award of state contracts and other benefits to the Gupta linked companies.

(iv) The investigation is conducted in terms of section 182 of the Constitution read with sections 6 and 7 of the Public Protector Act, 1994.

(v) In essence the allegations are as follows:

Key allegations

(vi) The investigation emanates from complaints lodged against the President by Father

S. Mayebe on behalf of the Dominican Order, a group of Catholic Priests, on 18 March 2016 (The First Complainant); Mr. Mmusi Maimane, the leader of the Democratic Alliance and Leader of the Opposition in Parliament on 18 March 2016 (The Second Complainant), in terms of section 4 of the Executive Members’ Ethics Act, 82 of 1998 (EMEA); and a member of the public on 22 April 2016 (The third Complainant), whose name I have withheld.

(vii) The complaints followed media reports alleging that the Deputy Minister of Finance, Hon. Mr. Mcebisi Jonas, was allegedly offered the post of Minister of Finance by the Gupta family long before his then colleague Mr. Nhlanhla Nene was abruptly removed by President Zuma on December 09, 2015. The post was allegedly offered to him by the Gupta family, which alleged has a long standing friendship with President Zuma’s family and a business partnership with his son Mr. Duduzane Zuma. The offer allegedly took place at the Gupta residence in Saxonwold, City of Johannesburg Gauteng. The allegation was that Ajay Gupta, the oldest of three Gupta brothers who are business partners of President Zuma’s son, Mr. Duduzane Zuma, in a company called Oakbay, among others, offered the position of Minister of Finance to Deputy Minister Jonas and must have influenced the subsequent removal of Minister Nene and his replacement with Mr. Des Van Rooyen on 09 December 2015, who was also abruptly shifted to the Cooperative Governance and Traditional Affairs portfolio 4 days later, following a public outcry.

(viii) The media reports also alleged that Ms. Vytjie Mentor was offered the post of Minister for Public Enterprises in exchange for cancelling the South African Airways (SAA) route to India and that President Zuma was at the Gupta residence when the offer was made and immediately advised about the same by Ms. Mentor. The media reports alleged that the relationship between the President and the Gupta family had evolved into “state capture” underpinned by the Gupta family having power to influence the appointment of Cabinet Ministers and Directors in Boards of SOEs and leveraging those relationships to get preferential treatment in state contracts, access to state provided business finance and in the award of business licenses.

(ix) Specific allegations were made and these are detailed below.

(x) The First Complainant, relying on media reports, requested an investigation into:

(a) The veracity of allegations that the Deputy Minister of Finance Mr Jonas and Ms Mentor (presumably as chairpersons of the Portfolio Committee of Public Enterprises) were offered Cabinet positions by the Gupta family;

(b) Whether the appointment of Mr Van Rooyen to Minister of Finance was known by the Gupta family beforehand;

(c) Media allegation that two Gupta aligned senior advisors were appointed to the National Treasury, alongside Mr Van Rooyen, without proper procedure; and

(d) All business dealings of the Gupta family with government departments and SOEs to determine whether there were irregularities, undue enrichment, corruption and undue influence in the awarding of contracts, mining licenses, government advertising in the New Age newspaper, and any other governmental services.

(xi) The second Complainant also relying on the same media reports, requested an investigation into the President’s role in the alleged offer of Cabinet positions to Deputy Minister Jonas and MP, Ms. Mentor, and that the investigation should look into the President’s conduct in relation to the alleged corrupt offers and Gupta family involvement in the appointment of Cabinet Ministers and Directors of SOE Boards.

(xii) In his complaint, Mr. Maimane stated amongst other things that:

“Section 2.3 of the Code of Ethics states that Members of the Executive may not:

(a) Willfully mislead the legislature to which they are accountable…(c) act in a way that is inconsistent with their position; (d) use their position or any information entrusted to them, to enrich themselves or improperly benefit any other person...” (my emphasis)

(b) It is our contention that President Jacob Zuma may have breached the Executive Ethics Code by (i) exposing himself to any situation involving the risk of a conflict between their official responsibilities and their private interests; (ii) acted in a way that is inconsistent with his position and (iii) use their position or any information entrusted to them, to enrich themselves or improperly benefit any other person”, he further stated. (my emphasis).

(xiii) The third complaint was also based on media reports but only those alleging that the Cabinet had decided to get involved in holding banks accountable for withdrawing banking facilities to Gupta owned companies. The Complainant wanted to know if it was appropriate for the Cabinet to assist a private business and on what grounds was that happening. He asked if corruption was not involved and specifically asked if such matters should not be dealt with by the National Consumer Commission or the Banking Ombudsman.

(xiv) While the investigation was conducted in terms of section 182 of the Constitution of the Republic of South Africa, 1996 (the Constitution), which confers the Public Protector power to investigate, report and take appropriate remedial action in response to alleged improper or prejudicial conduct in state affairs, the alleged improper conduct of President Zuma involving potential violation of the Executive Ethics Code, was principally investigated under section 3(1) of the Executive Ethics Code read with section 6 of the Public Protector Act. The provisions of the Prevention and Combatting of Corrupt Activities Act were invoked with regard to allegations regarding the alleged offer of a Ministerial position by the Gupta family to Ms. Mentor in return for cancelling the India route of the SAA, in the vicinity of President Zuma, and related allegations. Deputy Minister Jonas also alleged that the position offered was on condition that he works with the Gupta family and that too is in contravention of the Prevention and Combating of Corrupt Activities Act 12 of 2004 (PRECCA). The provisions of the Protected Disclosures Act, 26 of 2000 were also taken into account.

(xv) I decided to combine the complaints and have since conducted an investigation under section 182 of the Constitution which confers on the Public Protector the power to investigate any alleged or suspected improper or prejudicial conduct, to report on that conduct and to take appropriate remedial action; and in terms of section 3(1) of the EMEA which places a peremptory duty on the Public Protector to investigate allegations of unethical conduct or violations of the Executive Ethics Code by the President and other Members of the Executive. The Complaint is also investigated in terms of section 7(1) of the Public Protector Act, which regulates the Public Protector’s exercise of her/his investigative powers.

(xvi) Section 182(1) provides that:

The Public Protector has the power, as regulated by national legislation-

(a) to investigate any conduct in state affairs, or in the public administration in any sphere of government, that is alleged or suspected to be improper or to result in any impropriety or prejudice;

(b) to report on that conduct; and

(c) to take appropriate remedial action.

(xvii) Section 3(1) of the EMEA further provides that:

The Public Protector must investigate any alleged breach of the code of ethics on receipt of a complaint contemplated in section 4.

(xviii) The investigation was principally undertaken because of the Second Complainant having lodged his complaint under the EMEA, which does not allow the Public Protector discretionary power to consider whether or not to investigate a matter falling under his/her jurisdiction. Given that the Executive Members’ Ethics Act requires investigations under it to be concluded within 30 days, the investigation was given priority. It was also given priority because of the allegations having the potential of undermining public trust in the Executive and SOEs. Additional resources were requested from government with a view to handling it like a Commission of Inquiry and R1.5 million was allocated by the Department of Justice and Correctional Services for this purpose.

(xix) The investigation process was informed by the provisions of sections 6 and 7 of the Public Protector Act, 1994 (Public Protector Act). Section 6(4) recognises the power of the Public Protector to conduct own initiative investigations while section 6(5)(a) and (b) of the Public Protector Act specifically recognises the Public Protector’s investigate any maladministration in connection with the affairs of any institution in which the state is the majority or controlling shareholder or of any public entity as defined in section 1 of the Public Finance Management Act 1 of 1999 (PFMA); and abuse or unjustifiable exercise of power or unfair, capricious, discourteous or other improper conduct. Section 7 details the processes that may be followed, which involves an inquisitorial process that includes requests for information, subpoenas and interviews.

(xx) The complaint relates to allegations of improper conduct in state affairs and unethical conduct by the President of the Republic, and other state functionaries and accordingly falls within my ambit as the Public Protector. None of the parties challenged the jurisdiction of the Public Protector.

(xxi) Based on an analysis of the complaint, the following issues were identified as relevant for investigation:

Alleged breach of the Executive Member Ethics Act, 1998

a) Whether President Zuma improperly and in violation of the Executive Ethics Code, allowed members of the Gupta family and his son, to be involved in the process of removal and appointment of the Minister of Finance in December 2015;

b) Whether President Zuma improperly and in violation of the Executive Ethics Code, allowed members of the Gupta family and his son, to engage or be involved in the process of removal and appointing of various members of the Cabinet;

c) Whether President Zuma improperly and in violation of the Executive Ethics Code, allowed members of the Gupta family and his son, to be involved in the process of appointing members of Boards of Directors of SOEs;

d) Whether President Zuma has enabled or turned a blind eye, in violation of the Executive Ethics Code, to alleged corrupt practices by the Gupta family and his son in relation to allegedly linking appointments to quid pro quo conditions;

e) Whether President Zuma and other Cabinet members improperly interfered in the relationship between banks and Gupta owned companies thus giving preferential treatment to such companies on a matter that should have been handled by independent regulatory bodies;

f) Whether President Zuma improperly and in violation of the Executive Ethics Code exposed himself to any situation involving the risk of conflict between his official duties and his private interest or used his position or information entrusted to him to enrich himself and or enabled businesses owned by the Gupta family and his son to be given preferential treatment in the award of state contracts, business financing and trading licences; and

g) Whether anyone was prejudiced by the conduct of President Zuma.

Awarding of contracts by certain organs of state to entities linked to the Gupta family

a) Whether any state functionary in any organ of state or other person acted unlawfully, improperly or corruptly in connection with the appointment or removal of Ministers and Boards of Directors of SOEs;

b) Whether any state functionary in any organ of state or other person acted unlawfully, improperly or corruptly in connection with the award of state contracts or tenders to Gupta linked companies or persons;

c) Whether any state functionary in any organ of state or other person acted unlawfully, improperly or corruptly in connection with the extension of state provided business financing facilities to Gupta linked companies or persons;

d) Whether any state functionary in any organ of state or other person acted unlawfully, improperly or corruptly in connection with exchange of gifts in relation to Gupta linked companies or persons; and

e) Whether any person/entity was prejudiced due to the conduct of the said state functionary or organ of state.

Two Phased Inquisitorial Investigation Process

(xxii) The approach to the investigation was an inquisitorial process which asked questions raised about the President’s conduct: What happened? What should have happened? Is there a discrepancy between what happened and what should have happened and if there is a discrepancy, is it unjustifiable and material in the circumstances and if the President’s conduct qualifies to be regarded as improper conduct as alleged. The same approach was taken in relation to allegation of suspected conduct regarding awarding of tenders by SOEs and other organs of state and extension of other benefits to Gupta owned companies.

(xxiii) I must also indicate that the investigation has been divided into two phases and that the first phase of the investigation did not touch on the award of licenses to the Gupta family and superficially touched on state financing of the Gupta-Zuma business while only selecting a few state contracts. The division of work was to accommodate the time and resource limitations by addressing the pressing questions threatening to erode public trust in the Executive and SOEs while mapping the process for the second and final phase of the investigation.

(xxiv) The investigation process included correspondence with key parties implicated by the allegations and potential witnesses, with the President having been the first to be advised by myself in writing between March and April 2016, of the allegations being made and provided with copies of the first two complaints immediately after the complaints were lodged. President Zuma was also advised on 22 April 2016 and before the expiry of the mandatory 30 days for the completion of the investigation that it was not going to be possible to conclude the investigation within 30 days due to resources and communication challenges.

(xxv) Interviews were conducted with identified key witnesses, commencing with alleged whistle-blowers, Deputy Minister of Finance Mr Jonas and Ms Mentor, who confirmed their status as whistle-blowers. The investigation team also interviewed Mr Maseko, who was also identified by the media as a whistle-blower. Interviews were also conducted with several other ministers and other selected witnesses. Documents were requested from appropriate persons and institutions and analysed and evaluated together with the oral evidence to establish if any of the allegations could be corroborated. Towards the conclusion of the investigation persons who appeared to be implicated by the evidence collected by then were served with notices in terms of section 7(9) of the Public Protector Act to alert them of such evidence and the potential of adverse findings and afford them the opportunity to respond.

(xxvi) In that regard the following people were issued with notices in terms of section 7(9) of the Public Protect Act:

a) President Zuma on 2 October 2016;

b) Dr Ben Ngubane and the Board of Eskom on 4 October 2016;

c) Mr D. Zuma on 4 October 2016;

d) Mr Ajay Gupta on 4 October 2016;

e) Tegeta on 7 October 2016;

f) Minister Lynne Brown on 4 October 2016;

g) Minister Van Rooyen on 10 October 2016; and

h) Minister Mosebenzi Zwane 5 October 2016.

(xxvii) Regarding the standard that was expected of President Zuma as the President of South Africa and the sole custodian of Executive Authority of the republic, the provisions of sections 96, 195 and 237 of the Constitution were taken into account together with the provisions of the Executive Ethics Code, Section 6 of the Public Protector Act and general principles of good governance as outlined below.

(xxviii) The investigation process commenced by notification of President Zuma of the complaints received and that I intended to conduct a formal investigation into the complaints lodged. I also invited President Zuma to comment on the allegations. My investigation was conducted through meetings and interviews with the Complainants and witnesses as well as inspection of all relevant documents and analysis and application of all relevant laws, policies and related prescripts, followed.

(xxix) Key laws and policies taken into account to help me determine if there had been any improper and unethical conduct by the President and/or officials of the implicated State Organs due to their alleged inappropriate relationship with members of the Gupta family were principally those governing the conduct of members of the Executive (Executive Members Ethics Act, 1998 and Executive Ethics Code), the Constitution, policies governing procurement by the State and its organs, the Public Finance Management Act, the Companies Act King III Report on Corporate Governance, the Prevention and Combatting of Corrupt Activities Act and relevant National Treasury prescripts.

(xxx) Having considered the evidence uncovered during the investigation against the relevant regulatory framework, I make the following observations:

1. Regarding whether President Zuma improperly and in violation of the Executive Ethics Code, allowed members of the Gupta family and his son, to be involved in the process of removal and appointment of the Minister of Finance in December 2015:

(a) President Zuma was required to select and appoint Ministers lawfully and in compliance with the Executive Ethics Code.

(b) It is worrying that the the Gupta family was aware or may have been aware that Minister Nene was removed 6 weeks after Deputy Minister Jonas advised him that he had been allegedly offered a job by the Gupta family in exchange for extending favours to their family business.

(c) Equally worrying is that Minister Van Rooyen who replaced Minister Nene can be placed at the Saxonwold area on at least seven occasions including on the day before he was announced as Minister. This looks anomalous given that at the time he was a Member of Parliament based in Cape Town.

(d) Furthermore one of the two advisers he brought with to National Treasury on his first day at work, 11 October 2015 had contact with someone at the Saxonwold area the day before.

(e) The coincidence is a source of great concern.

(f) Another worrying coincidence is that Minister Nene was removed after Mr Jonas advised him that he was going to be removed.

(g) If the Gupta family knew about the intended appointment it would appear that information was shared then in violation of section 2.3(e) of the Executive Ethics Code which prohibits members of the executive from the use of information received in confidence in the course of their duties or otherwise than in connection with the discharge of their duties.

(h) The provision of Section 2.3(c) which prohibits a member of the Executive from acting in a way that is inconsistent with their position. There might even be a violation of Section 2.3(e) of the Executive Ethics Code which prohibits a member of the Executive from using information received in confidence in the course of their duties otherwise than in connection with the discharge of their duties.

(i) In view of the fact that the allegation that was made public included Mr Jonas alleging that the offer for a position of Minister was linked to him being required to extend favours to the Gupta family. Failure to verify such allegation may infringe the provisions of Section 34 of Prevention and Combatting of Corrupt Activities Act, 12 of 2004 which places a duty on persons in positions of authority who knows or ought reasonably to have known or suspected that any other person has committed an offence under the Act must report such knowledge or suspicion or cause such knowledge or suspicion to be reported to any police official.

2. Regarding whether President Zuma improperly and in violation of the Executive Ethics Code, allowed members of the Gupta family and his son, to engage or to be involved in the process of removal and appointing of various members of Cabinet

(a) There seems to be no evidence of action taken by anyone to verify Ms Mentor’s allegation(s). If this observation is true, the provisions of Section 195 of the Constituion as interpreted in Khumalo v MEC for Education, KZN would not have been complied with. If this is the case, the provision of Section 2.3(c) which prohibits a member of the Executive from acting in a way that is inconsistent with their position, is applicable. There might even be a violation of Section 2.3(e) of the Executive Ethics Code which prohibits a member of the Executive from using information received in confidence in the course of their duties otherwise than in connection with the discharge of their duties. In view of the fact that the allegation that was made public included Mr Jonas alleging that the offer for a position of Minister was linked to him being required to extend favours to the Gupta family, failure to verify such allegation may infringe the provisions of Section 34 of Prevention and Combatting of Corrupt Activities Act, 12 of 2004 which places a duty on persons in positions of authority who knows or ought reasonably to have known or suspected that any other person has committed an offence under the Act must report such knowledge or suspicion or cause such knowledge or suspicion to be reported to any police official.

3. Whether President Zuma improperly and in violation of the Executive Ethics Code, allowed members of the Gupta family and his son, to be involved in the process of appointing members of Board of Directors of SOEs

(a) A similar duty is imposed and possibly violated in relation to the allegations that were made by Mr Maseko about his removal. The same to applies to persistent allegations regarding an alleged cozy relationship between Mr Brian Molefe and the Gupta family. In this case it is worth noting that such allegations are backed by evidence and a source of concern that nothing seems to have been done regardless of the duty imposed by Section 195 of the Constitution on relevant State functionaries.

(b) While not relevant to the alleged influence of the Gupta family, the allegations made by Ms Hogan also deserve a closer look to the extent that they suggest Executive and party interference in the management of SOEs and appointments thereto.

4. Whether President Zuma has enabled or turned a blind eye, in violation of the Executive Ethics Code, to alleged corrupt practices by the Gupta family and his son in relation to allegedly linking appointments to quid pro quo conditions

(a) There seems to be no evidence showing that Mr Jonas’ allegations that he was offered money and a ministerial post in exchange for favours were ever investigated by the Executive. Only the African National Congress and Parliament seemed to have considered this worthy of examination or scrutiny.

(b) If this observation is correct then the provisions of section 2.3 (c) of the Executive Ethics Code may have been infringed as alleged.

5. Regarding whether President Zuma and other Cabinet members improperly interfered in the relationship between banks and Gupta owned companies thus giving preferential treatment to such companies on a matter that should have been handled by independent regulatory bodies;

(a) Cabinet appears to have taken an extraordinary and unprecedented step regarding intervention into what appears to be a dispute between a private company co owned by the President’s friends and his son. This needs to be looked at in relation to a possible conflict of interest between the President as head of state and his private interest as a friend and father as envisaged under section 2.3(c) of the Executive Ethics Code which regulates conflict of interest and section 195 of the Constitution which requires a high level of professional ethics. Sections 96(2)(b) and (c) of the Constitution are also relevant.

6. Whether President Zuma improperly and in violation of the Executive Ethics Code exposed himself to any situation involving the risk of conflict between his official duties and his private interest or use his position or information entrusted to him to enrich himself and businesses owned by the Gupta family and his son to be given preferential treatment in the award of state contracts, business financing and trading licences

(a) The allegations raised by both Messrs Jonas and Maseko are relevant as is action taken and/or not taken in relation thereto.

7. Whether anyone was prejudiced by the conduct of President Zuma

(a) Deputy Minister Jonas would be regarded as a liar and publicly humiliated unless he is vindicated in his public statement that Mr Ajay Gupta offered the position of Minister of Finance to him with the knowledge of President Zuma who subsequently denied such offer. Consequently the people of South Africa, who Deputy Minister Jonas took into his confidence in revealing this, would lose faith in open, democratic and accountable government if President Zuma’s denials are proven to be false.

8. Whether any state functionary in any organ of state or other person acted unlawfully, improperly or corruptly in connection with the appointment or removal of Ministers and Boards of Directors of SOEs

(a) It appears that the Board at Eskom was improperly appointed and not in line with the spirit of the King III report on good Corporate Governance.

(b) Even though certain conflicts may have arisen after the Board was appointed, there should have been a mechanism in place to deal with the conflicts as they arose and managed actual or perceived bias.

(c) A Board appointed to an SOE, is expected to act in the best interests of the Republic of South Africa at all times and it appears that the Board may have failed to do so.

(d) It appears as though no action was taken on the part of the Minister of Public Enterprise as Government stakeholder to prevent these apparent conflicts.

9. Whether any state functionary in any organ of state or other person acted unlawfully, improperly or corruptly in connection with the award of state contracts or tenders to Gupta linked companies or persons

(a) Minister Zwane’s conduct with regards to his flight itinerary to Switzerland appears to be irregular. This may not be in line with the PFMA.

(b) It appears that Minister Zwane’s conduct may not be in line with section 96(2) of the Constitution and section 2 of the Executive Members Ethics Act.

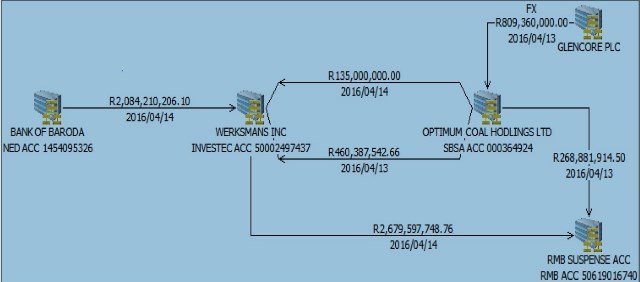

(c) In light of the extensive financial analysis conducted, it appears that the sole purpose of awarding contracts to Tegeta to supply Arnot Power Station, was made solely for the purposes of funding Tegeta and enabling Tegeta to purchase all shares in OCH. The only entity which appears to have benefited from Eskom’s decisions with regards to OCM/OCH was Tegeta which appears to have been enabled to purchase all shares held in OCH. The favourable payment terms given to Tegeta (7 days) need to be examined further. OCM clearly had 30 day payment terms with Tegeta for the supply of coal to Arnot Power Station, and Eskom appears to have been aware of this. It also appears that Tegeta did not meet all its obligations to OCM as OCM was owed R 148,027,783.91 by Tegeta as at 31 July 2016 and an amount of R 289,842,376.00 as at 31 August 2016.

(d) This may amount to a possible contravention of section 38 and 51 of the PFMA which states that a Board needs to prevent fruitless and wasteful expenditure, which in turn is an act of financial misconduct under section 83(1)(a) of the PFMA and subject to the penalties under section 86(2) of the PFMA.

(e) It appears that the Eskom Board did not exercise a duty of care, which may constitute a violation of section 50 of the PFMA.

(f) Eskom’s awarding of the initial contracts to Tegeta to supply coal to the Majuba Power Station will form part of the next phase of the investigation.

10. Whether any state functionary in any organ of state or other person acted unlawfully, improperly or corruptly in connection with the extension of state provided business financing facilities to Gupta linked companies or persons;

(a) The prepayment to Tegeta in the amount R659 558 079.00 (six hundred and fifty nine million five hundred and fifty eight thousand seventy nine rand) inclusive of VAT, may not be in line with the PFMA. This is evidenced in the BRP’s section 34 report in which it is stated that the prepayment was not used to fund OCM, it is further emphasised in the financial analysis which shows the prepayment was used entirely for the purposes of funding the purchase of all shares in OCH. On 11 April 2016, Tegeta informed the BRP’s and Glencore, who in turn informed the Loan Consortium that they were R600 million short, on the very same day, Eskom held an urgent Board Tender Committee meeting at 21:00 in the evening to approve the prepayment which was R659 558 079.00 (six hundred and fifty nine million five hundred and fifty eight thousand seventy nine rand and 38 cents) inclusive of VAT.

(b) The Eskom Board does not appear to have exercised a duty of care or acted, which may constitute a violation of section 50 of the PFMA.

(c) Tegeta’s conduct and misrepresentations made to the public with regards to the prepayment and the actual reason for the prepayment could amount to fraud. Furthermore, the shareholders of Tegeta (Oakbay, Mabengela, Fidelity, Accurate and Elgasolve) pledged their shares to Eskom in respect of the prepayment and thus knew of the nature of the transaction.

(d) It appears that the manner in which the rehabilitation funds are currently being handled with the Bank of Baroda, are in contravention of section 24P of NEMA as well as section 7 of the financial regulations which provide that that the financial provision must be “equal to the sum of the actual costs of implementing the plans and report contemplated in regulation 6 and regulation 11(1) for a period of at least 10 years forthwith”. This cannot be guaranteed by the Bank of Baroda or Tegeta as the funds are consistently moved around between accounts as well as other branches, Tegeta accordingly may have contravened section 7 of the financial regulations which is an offence under section 18 of the financial regulations which in turn is liable to a fine not exceeding R10 million or to imprisonment not exceeding 10 years or to both.

(e) According to the Financial Provision Regulations (“Financial Regulations”), where an applicant or holder of a right or permit makes use of the financial vehicle as contemplated in regulation 9(5) read with 8(1) (b), any interest earned on the deposit shall first be used to defray bank charges in respect of that account and thereafter accumulate and form part of the financial provision. In neither of the funds held in the Bank of Baroda accounts was the interest reinvested for the purposes of capital growth. The interest is transferred back into the Bank of Baroda account and utilised. It seems as if the interest serves as a direct benefit to the Bank of Baroda and not the owner of the invested funds as it would be in terms of a normal capital investment. Tegeta may have contravened section 9(5) of the financial regulations.

By not treating the rehabilitations funds in the prescribed manner and for the prescribed purpose, Tegeta is in contravention of section 37A of the Income Tax Act. The Commissioner may include an amount equal to twice the market value of all property held in the rehabilitation fund, on the date of contravention, in the rehabilitation fund's taxable income, and include the amount that the mining company contributed to the rehabilitation fund (and claimed a tax deduction for), in the mining company's income, to the extent that the property in the rehabilitation fund was directly or indirectly derived from cash paid to the rehabilitation fund.

(f) The Commissioner may include an amount equal to twice the market value of all property held in the rehabilitation fund, on the date of contravention, in the rehabilitation fund's taxable income, and include the amount that the mining company contributed to the rehabilitation fund (and claimed a tax deduction for), in the mining company's income, to the extent that the property in the rehabilitation fund was directly or indirectly derived from cash paid to the rehabilitation fund. This is potentially a sum of double the amount of R280.000.000.00 which was available in the KRTF and a sum of double the amount R1,469.916.933.63 which was available in the ORTF.

(g) The Bank of Baroda in relation to the purchase of all shares in OCH by Tegeta and the rehabilitation fund. This will form part of the next phase of the investigation.

11. Whether any state functionary in any organ of state or other person acted unlawfully, improperly or corruptly in connection with exchange of gifts in relation to Gupta linked companies or persons;

(a) This issue will be attended to further in the next phase of the investigation.

12. Whether any person/entity was prejudiced due to the conduct of the SOE.

(a) Eskom may have numerous methods caused prejudiced to Glencore. Glencore appears to have been severely prejuidiced by Eskom’s actions in refusing to sign a new agreement with them for the supply of coal to Hendrina Power Station, this was not in line with previous discussions held by Glencore with Eskom, furthermore, it is unclear as to why approval was needed from the Acting Chief Executive before the agreement was signed, as the necessary approvals appear to already have been obtained. It appears that the conduct of Eskom, was solely for the purposes of forcing OCM/OCH into business rescue and financial distress.

(b) It appears that the conduct of Eskom was solely to the benefit of Tegeta, in that they forced the sale of OCH to Tegeta by stating that OCM could be sold alone. Thereafter, it appears, they have allowed Tegeta to proceed with the sale of a portion of OCH in the form of the Optimum Coal Terminal. This may constitute a contravention of section 50(2) of the PFMA in that they acted solely for the benefit of one company.

(xxxi) The appropriate remedial action I am taking in pursuit of section 182(1)(c) of the Constitution, with the view of placing the Complainant as close as possible to where he would have been had the improper conduct or maladministration not occurred, while addressing systemic procurement management deficiencies in the Department, is the following:

(a) The investigation has proven that the extent of issues it needs to traverse and resources necessary to execute it is incapable of being executed fully by the Public Protector. This was foreshadowed at the commencement of the investigation when the Public Protector wrote to government requesting for resources for a special investigation similar to a commission of inquiry overseen by the Public Protector. This investigation has been hamstrung by the late release which caused the investigation to commence later than planned. The situation was compounded by the inadequacy of the allocated funds (R1.5 Million).

(b) The President has the power under section 84(2)(f) of the Constitution to appoint commissions of enquiry however, in the EFF Vs Speaker of Parliament the President said that: “I could not have carried out the evaluation myself lest I be accused of being judge and jury in my own case”.

(c) The President to appoint, within 30 days, a commission of inquiry headed by a judge solely selected by the Chief Justice who shall provide one name to the President.

(d) The judge to be given the power to appoint his/her own staff and to investigate all the issues using the record of this investigation and the report as a starting point.

(e) The President to ensure that the commission is adequately resourced, in conjuction with the National Treasury.

(f) The commission of inquiry to be given powers of evidence collection that are no less than that of the Public Protector.

(g) The commission of inquiry to complete its task and to present the report with findings and recommendations to the President within 180 days. The President shall submit a copy with an indication of his/her intentions regarding the implementation to Parliament within 14 days of releasing the report,

(h) Parliament to review, within 180 days, the Executive Members’ Ethics Act to provide better guidance regarding integrity, including avoidance and management of conflict of interest. This should clearly define responsibilities of those in authority regarding a proper response to whistleblowing and whistleblowers. Consideration should also be given to a transversal code of conduct for all employees of the State.

(i) The President to ensure that the Executive Ethics Code is updated in line with the review of the Executive Members’ Ethics Act.

(j) The Public Protector, in terms of section 6 (4) (c) (i) of the Public Protector Act, brings to the notice of the National Prosecuting Authority and the DPCI those matters identified in this report where it appears crimes have been committed.

INVESTIGATION INTO COMPLAINTS OF ALLEGED IMPROPER AND UNETHICAL CONDUCT BY THE PRESIDENT AND OTHER STATE FUNCTIONARIES RELATING TO ALLEGED IMPROPER RELATIONSHIPS AND INVOLVEMENT OF THE GUPTA FAMILY IN THE REMOVAL AND APPOINTMENT OF MINISTERS AND DIRECTORS OF SOES RESULTING IN IMPROPER AND POSSIBLY CORRUPT AWARD OF STATE CONTRACTS AND BENEFITS TO THE GUPTA FAMILY’S BUSINESSES

1. INTRODUCTION

1.1. “State of Capture” is my report in terms of section 182(1)(b) of the Constitution of the Republic of South Africa, 1996 (the Constitution) and section 8(1) of the Public Protector Act, 1994 (the Public Protector Act) and Section 3(1) of the Executive Members Act, 1998.

1.2. The report is submitted in terms of section 8(1) of the Public Protector Act, to:

a) The Speaker of the National Assembly, the Honourable Baleka Mbete;

b) The Director General in the Presidency and Secretary of Cabinet, Dr Cassius Lubisi;

c) Board of Directors of Eskom SOC Limited; and

d) The Minister of the Department of Public Enterprises, Ms Lynne Brown.

1.3. A copy of the report will also be provided to the Complainants in terms of section 8(3) of the Public Protector Act, namely:

a) Father S Mayebe; and

b) Honourable Mmusi Maimane, MP.

1.4. A copy of the report will further be provided to the following persons in terms of Section 8(3) of the Public Protector Act:

a) The President of the Republic His Excellency J.G Zuma;

b) Mr D. Zuma;

c) Mr Ajay Gupta;

d) Mr Atul Gupta;

e) Mr Rajesh Gupta;

f) Mr Hlongwane;

g) Minister Zwane;

h) Minister Van Rooyen; and

i) Minister Mbalula.

1.5. A copy of the report will further be provided to the following persons in terms of Section 6(4)(c)(i) of the Public Protector Act:

a) The National Director of Public Prosecutions, Adv Shaun Abrahams;

b) The Head of the Directorate for Priority Crimes Investigation, Brig. Berning Ntlemeza

1.6. This report relates to an investigation into complaints of alleged improper and unethical conduct by the president and other state functionaries relating to alleged improper relationships and involvement of the Gupta family in the removal and appointment of ministers and directors of State Owned Entities (SOEs) resulting in improper and possibly corrupt award of state contracts and benefits to the Gupta family’s businesses.

2. THE COMPLAINT

2.1. The Public Protector received three complaints in connection with the alleged improper and unethical conduct relating to the appointments of Cabinet Ministers.

2.2. The investigation was conducted in terms of section 182 of the Constitution read with sections 6 and 7 of the Public Protector Act, 1994.

2.3. In essence the allegations are as follows:

Key allegations

2.4. The investigation emanates from complaints lodged against the President by Father

S. Mayebe on behalf of the Dominican Order, a group of Catholic Priests, on 18 March 2016 (The First Complainant); Mr. Mmusi Maimane, the leader of the Democratic Alliance and Leader of the Opposition in Parliament on 18 March 2016 (The Second Complainant), in terms of section 4 of the Executive Members’ Ethics Act, 82 of 1998 (EMEA); and a member of the public on 22 April 2016 (The third Complainant), whose name I have withheld.

2.5. The complaints followed media reports alleging that the Deputy Minister of Finance, Hon. Mr. Mcebisi Jonas, was allegedly offered the post of Minister of Finance by the Gupta family long before his then colleague Mr. Nhlanhla Nene was abruptly removed by the President on December 09, 2015. The post was offered to him by the Gupta family, which has a long standing friendship with President Zuma’s family and a business partnership with his son Mr. Duduzane Zuma. The offer took place at the Gupta residence in Saxonwold, City of Joburg Gauteng. The allegation was that Atul Gupta, the oldest of three Gupta brothers who are business partners of President Zuma’s son, Mr. Duduzane Zuma, in a company called Oakbay, among others, offered the position of Minister of Finance to Deputy Minister Jonas and must have influenced the subsequent removal of Minister Nene and his replacement with Mr. Des Van Rooyen on 09 December 2015, who was also abruptly shifted to the Cooperative Governance and Traditional Affairs portfolio 4 days later, following a public outcry.

2.6. The media reports also alleged that Ms. Vytjie Mentor was offered the post of Minister for Public Enterprises in exchange for cancelling the South African Airways (SAA) route to India and that President Zuma was at the Gupta residence when the offer was made and immediately advised about the same by Ms. Mentor. The media reports alleged that the relationship between the President and the Gupta family had evolved into “state capture” underpinned by the Gupta family having power to influence the appointment of Cabinet Ministers and Directors in Boards of SOEs and leveraging those relationships to get preferential treatment in state contracts, access to state provided business finance and in the award of business licenses.

2.7. Specific allegations were made, which are detailed below.

2.8. The First Complainant, relying on media reports, requested an investigation into:

a) The veracity of allegations that the Deputy Minister of Finance Mr Jonas and Ms Mentor (presumably as chairpersons of the Portfolio Committee of Public Enterprises) were offered Cabinet positions by the Gupta family;

b) Whether the appointment of Mr Van Rooyen to Minister of Finance was known by the Gupta family beforehand;

c) Media allegation that two Gupta aligned senior advisors were appointed to the National Treasury, alongside Mr Van Rooyen, without proper procedure; and

d) All business dealings of the Gupta family with government departments and SOEs to determine whether there were irregularities, undue enrichment, corruption and undue influence in the awarding of contracts, mining licenses, government advertising in the New Age newspaper, and any other governmental services.

2.9. The second Complainant also relying on the same media reports, requested an investigation into the President’s role in the alleged offer of Cabinet positions to Deputy Minister Jonas and MP, Ms. Mentor, and that the investigation should look into the President’s conduct in relation to the alleged corrupt offers and Gupta family involvement in the appointment of Cabinet Ministers and Directors of SOE Boards.

2.10. In his complaint, Mr. Maimane stated amongst other things that:

“Section 2.3 of the Code of Ethics states that Members of the Executive may not:

(a) Willfully mislead the legislature to which they are accountable…(c) act in a way that is inconsistent with their position; (d) use their position or any information entrusted to them, to enrich themselves or improperly benefit any other person...”

(b) It is our contention that President Jacob Zuma may have breached the Executive Ethics Code by (i) exposing himself to any situation involving the risk of a conflict between their official responsibilities and their private interests; (ii) acted in a way that is inconsistent with his position and (iii) use their position or any information entrusted to them, to enrich themselves or improperly benefit any other person”, he further stated.

2.11. The third complaint was also based on media reports but only those alleging that the Cabinet had decided to get involved in holding banks accountable for withdrawing banking facilities for Gupta owned companies. The Complainant wanted to know if it was appropriate for the Cabinet to assist a private business and on what grounds was that happening. He asked if corruption was not involved and specifically asked if such matters should not be dealt with by the National Consumer Commission or the Banking Ombudsman.

2.12. While the investigation was conducted in terms of section 182 of the Constitution of the Republic of South Africa, 1996 (the Constitution), which confers on the Public Protector the power to investigate, report and take appropriate remedial action in response to alleged improper or prejudicial conduct in state affairs, the alleged improper conduct of President Zuma involving potential violation of the Executive Ethics Code, was principally investigated under section 3(1) of the Executive Ethics Code. The provisions of the Prevention and Combatting of Corrupt Activities Act were invoked with regard to allegations regarding the alleged offer of a Ministerial position by the Gupta family to Ms. Mentor in return for cancelling the India route of the SAA, in the vicinity of President Zuma, and related allegations. The provisions of the Protected Disclosures Act were also taken into account.

2.13. I decided to combine the complaints and have since conducted an investigation under section 182 of the Constitution which confers on the Public Protector the power to investigate any alleged or suspected improper or prejudicial conduct, to report on that conduct and to take appropriate remedial action; and in terms of section 3(1) of the EMEA which places a peremptory duty on the Public Protector to investigate allegations of unethical conduct or violations of the Executive Ethics Code by the President and other Members of the Executive. The Complaint is also investigated in terms of section 7(1) of the Public Protector Act, which regulates the Public Protector’s exercise of her/his investigative powers.

2.14. The investigation was principally undertaken because of the Second Complainant having lodged his complaint under the EMEA, which does not allow the Public Protector discretionary power to consider whether or not to investigate a matter falling under his/her jurisdiction. Section 3(1) of the EMEA states that given that the Executive Members’ Ethics Act requires investigations under it to be concluded within 30 days, the investigation was given priority. It was also given priority because of the allegations having the potential of undermining public trust in the Executive and SOEs. Additional resources were requested from government with a view to handling it like a Commission of Inquiry and R1.5 million was allocated by the Department of Justice and Correctional Services for the purpose.

2.15. The investigation process was informed by the provisions of sections 6 and 7 of the Public Protector Act, 1994 (Public Protector Act). Section 6(4) empowers the Public Protector to conduct own initiative investigations while section 6(5) (a) and (b) of the Public Protector Act specifically empowers the Public Protector to investigate any maladministration in connection with the affairs of any institution in which the state is the majority or controlling shareholder or of any public entity as defined in section 1 of the Public Finance Management Act, No. 1 of 1999 (PFMA); and abuse or unjustifiable exercise of power or unfair, capricious, discourteous or other improper conduct. Section 7 details the processes that may be followed, which involves an inquisitorial process that includes requests for information, subpoenas and interviews.

2.16. The complaint relates to allegations of improper conduct in state affairs and unethical conduct by the President of the Republic, and accordingly falls within my ambit as the Public Protector.

2.17. Based on an analysis of the complaint, the following issues were identified as relevant for investigation:

Alleged breach of the Executive Member Ethics Act, 1998

a) Whether President Zuma improperly and in violation of the Executive Ethics Code, allowed members of the Gupta family and his son, to be involved in the process of removal and appointment of the Minister of Finance in December 2015;

b) Whether President Zuma improperly and in violation of the Executive Ethics Code, allowed members of the Gupta family and his son, to engage or be involved in the process of removal and appointing of various members of Cabinet;

c) Whether President Zuma improperly and in violation of the Executive Ethics Code, allowed members of the Gupta family and his son, to be involved in the process of appointing members of Boards of Directors of SOEs;

d) Whether President Zuma has enabled or turned a blind eye, in violation of the Executive Ethics Code, to alleged corrupt practices by the Gupta family and his son in relation to allegedly linking appointments to quid pro quo conditions;

e) Whether President Zuma and other Cabinet members improperly interfered in the relationship between banks and Gupta owned companies thus giving preferential treatment to such companies on a matter that should have been handled by independent regulatory bodies;

f) Whether President Zuma improperly and in violation of the Executive Ethics Code exposed himself to any situation involving the risk of conflict between his official duties and his private interest or use his position or information entrusted to him to enrich himself and businesses owned by the Gupta family and his son to be given preferential treatment in the award of state contracts, business financing and trading licences; and

g) Whether anyone was prejudiced by the conduct of President Zuma.

Awarding of contracts by certain State Owned Entities to entities linked to the Gupta family

a) Whether any state functionary in any organ of state or other person acted unlawfully, improperly or corruptly in connection with the appointment or removal of Ministers and Boards of Directors of SOEs;

b) Whether any state functionary in any organ of state or other person acted unlawfully, improperly or corruptly in connection with the award of state contracts or tenders to Gupta linked companies or persons;

c) Whether any state functionary in any organ of state or other person acted unlawfully, improperly or corruptly in connection with the extension of state provided business financing facilities to Gupta linked companies or persons;

d) Whether any state functionary in any organ of state or other person acted unlawfully, improperly or corruptly in connection with exchange of gifts in relation to Gupta linked companies or persons; and

e) Whether any person/entity was prejudiced due to the conduct of the SOE.

Two Phased Inquisitorial Investigation Process

2.18. The approach to the investigation was an inquisitorial process which asked questions about conduct: What happened? What should have happened? Is there a discrepancy between what happened and what should have happened and if there is a discrepancy, is it unjustifiable and material in the circumstances and if the conduct qualifies to be regarded as improper conduct as alleged.

2.19. I must also indicate that the investigation has been divided into two phases and that the first phase of the investigation did not touch on the award of licenses to the Gupta family and superficially touched on state financing of the Gupta-Zuma business while only selecting a few state contracts. The division of work was to accommodate the time and resource limitations by addressing the pressing questions threatening to erode public trust in the Executive and SOEs while mapping the process for the second and final phase of the investigation.

2.20. The investigation process included correspondence with key parties implicated by the allegations and potential witnesses, with the President having been the first to be advised by myself in writing of the allegations being made and provided with copies of the first two complaints immediately after the complaints were lodged. President Zuma was also advised before the expiry of the mandatory 30 days for the completion of the investigation that it was not going to be possible to conclude the investigation within 30 days due to resources and communication challenges.

2.21. Interviews were conducted with identified key witnesses, commencing with alleged whistle-blowers, Deputy Minister of Finance Mr Jonas and Ms Mentor, who confirmed their status as whistle-blowers. The investigation team also interviewed Mr Maseko, who was also identified by the media as a whistle-blower. Interviews were also conducted with several other ministers other selected witnesses. Documents were requested from appropriate persons and institutions and analysed and evaluated together with the oral evidence to establish if any of the allegations could be corroborated.

2.22. Regarding the standard that was expected of President Zuma as the President of South Africa and the sole custodian of Executive Authority of the republic, the provisions of sections 96, 195 and 237 of the Constitution taken into account together with the provisions of the Executive Ethics Code, Section 6 of the Public Protector Act and general principles of good governance as outlined below.

2.23. The investigation process commenced by notification of President Zuma of the complaints received and that I intended to conduct a formal investigation into the complaints lodged. I also invited President Zuma to comment on the allegations. My investigation was conducted through meetings and interviews with the Complainants and witnesses as well as inspection of all relevant documents and analysis and application of all relevant laws, policies and related prescripts, followed.

2.24. Key laws and policies taken into account to help me determine if there had been any improper and unethical conduct by the President and/or officials of the implicated State Organs due their alleged inappropriate relationship with members of the Gupta family were principally those governing the conduct of members of the Executive (Executive Members Ethics Act, 1998 and Executive Ethics Code), the Constitution, policies governing procurement by the respective State and its Organs, the Public Finance Management Act, the Companies Act, King III Report on Corporate Governance, Prevention and Combatting of Corrupt Activities Act, Mineral and Petroleum Resources Development Act, 28 of 2002 and relevant National Treasury prescripts.

3. POWERS AND JURISDICTION OF THE PUBLIC PROTECTOR

3.1. The Public Protector was established under section 181(1)(b) of the Constitution to strengthen constitutional democracy through investigating and redressing improper conduct in state affairs.

3.2. Section 182(1) of the Constitution provides that the Public Protector has the power to investigate any conduct in state affairs, or in the public administration in any sphere of government, that is alleged or suspected to be improper or to result in any impropriety or prejudice, to report on that conduct and take appropriate remedial action. Section 182(2) directs that the Public Protector has additional powers prescribed in legislation.

3.3. The Public Protector is further empowered by the Public Protector Act to investigate and redress maladministration and related improprieties in the conduct of state affairs and to resolve the disputes through conciliation, mediation, negotiation or any other appropriate alternative dispute resolution mechanism.

3.4. The conduct of the President of the Republic in so far as his official duties are concerned amounts to conduct in State Affairs and as a result, the matter falls within the ambit of the Public Protector.

3.5. Eskom SOC Limited is a State Owned Entity as listed under Schedule 2 of the Public Finance Management Act, Act No.1 of 1999 and its conduct amounts to conduct in state affairs and as a result, the matter falls within the ambit of the Public Protector.

3.6. The Public Protector’s jurisdiction to investigate was not disputed by any of the parties. However, the Public Protector’s powers of subpoena were questioned by the Secretary General of the African National Congress (“ANC”), Mr Gwede Mantashe and the President of the ANC Youth League (“ANCYL”), Mr Collen Maine (“Mr Maine”).

3.7. Mr Maine and Mr Mantashe questioned the Public Protector’s powers of subpoena to private persons and organisations / institutions.

3.8. I responded to Messrs Mantashe and Maine by referring them to relevant sections of the Public Protector Act. Section 7(4)(a) of the Public Protector Act stipulates that “the Public Protector may direct any person to assist her in any investigation. Section 7(4)(a) also provides that: “For the purposes of conducting an investigation, the Public Protector may direct any person to submit an affidavit or affirmed declaration or to appear before him or her to give evidence or to produce any document in his or her possession or under his or her control which has a bearing on the matter being investigated, and may examine such person.”

3.9. I highlighted to both Messrs Mantashe and Maine that the above sections of the Act essentially mean that while the Public Protector’s powers and jurisdiction is to investigate malfeasance in whatever form in state affairs, however in pursuit of this constitutional duty the Public Protector is empowered to enlist the assistance of any person.

3.10. Subsequent to the above, Mr Mantashe agreed to assist and Mr Maine never responded.

Legal interactions between myself and persons implicated in the investigation

President Zuma

3.11. On 22 March 2016 I wrote to President Zuma advising that I had received a request from the Democratic Alliance to conduct an investigation into the alleged breach of the Executive Member’s Code of Ethics by President Zuma for his alleged role in the offering of Ministerial positions by members of the Gupta family. I quoted relevant extracts from the complaint and the Executive Member’s Ethics Act. I attached the complaint itself. I asked the President “if you have any comments on the allegations levelled against you, I will appreciate a letter indicating such comments from you.”

3.12. In the same letter I advised President Zuma that I had received a request from the Dominican Order to conduct a systemic investigation into undue influence in Minister’s and Deputy Minister’s appointments, possible corruption, undue enrichment and undue influence in the award of tenders, mining licences and government advertisements. I attached the complaint itself. I again asked the President “should you have a comment thereon or information that can assist, kindly forward the same to me as soon as possible.”

3.13. On 22 April 2016 I forwarded a copy of my letter dated 22 March 2016 to President Zuma (which had apparently not reached the President). I advised that I was required to submit a report on the alleged breach of the Executive Member’s Code of Ethics within 30 days of receipt of the complaint. I reported to the President that the investigation had not been completed due to inadequate resources.

3.14. I received no response from the President.

3.15. By early September 2016 my office had received additional funds in order to proceed with the investigation.

3.16. On 13 September 2016 I sent another letter to the President asking for a meeting with him in order to brief him on the investigation and affording him a further opportunity to comment on the allegations, which were summarised to the effect that the President ought to have known and/or allowed his son Duduzane Zuma to exercise enormous undue influence in strategic ministerial appointments as well as board appointments at SOEs.

3.17. On 1 October 2016 I sent President Zuma a Notice in terms of Section 7 (9) of the Public Protector Act. The notice restated the complaints and added the third complaint. I advised that my investigation was now being conducted in terms of section 182 of the Constitution read with sections 6 and 7 of the Public Protector Act. I provided a full description of the issues investigated and how President Zuma was implicated therein. I detailed the evidence implicating President Zuma before describing his responsibility under law. I ended off the notice by advising the President that if I do not get his version which contradicts the said evidence, there would be a possibility that I could find that the above allegations are sustained by the evidence. I detailed the various conclusions that I would make in that case.

3.18. In the meantime, a meeting was scheduled with the President for 6 October 2016.

3.19. On 5 October 2016 I received a letter from the Office of the Presidency referring to a media article and asking, in preparation for the meeting, for urgent advice on the findings I had made as well as a report on whether the veracity of the allegations by Jonas had been fully ventilated and investigated.

3.20. On 6 October 2016 I met with the President, whose legal team raised various legal objections and refused to discuss the merits of the investigation or the allegations against the President. The Presidency requested that the meeting be postponed to allow the President to study the documents provided and obtain legal advice. The Presidency raised an objection that they had not been provided with the relevant documents and records, and argued that they should be allowed to question witnesses who had already testified before me. I disagreed with this request and instead offered to provide the President with written questions to which the President would be required to respond by affidavit.

3.21. The President’s legal advisor argued emphatically that the matter should be deferred to the incoming Public Protector for conclusion. There was a lengthy discussion with the President and his advisor on this matter, after which the President expressed his willingness to answer the questions posed by the Public Protector, at a future date, after having had an opportunity to scrutinize the documents and consult with his legal advisor. I advised the President that as head of state, he is accountable to the people of the Republic, and that it is in his interest that he do so. In an attempt to demonstrate to the President that my questions to him were questions of fact, not requiring legal assistance, I posed said questions to him. This discussion is captured in the transcript of this meeting, which is attached hereto as Annexure 11. The President undertook to meet with me again on 10 October 2016 and provide me with an affidavit in response to the questions posed.

3.22. On 10 October 2016 I received a letter from the Presidency, in which he took exception to having been given two days before the meeting of 6 October 2016 to prepare for and give evidence on a range of matters which exceeded the ambit of the stated request for the meeting. This was as a result of the Notice in terms of Section 7(9) having only been received on 2 October 2016.

3.23. The letter continued to raise issues of objection. Firstly, the Presidency advised that Section 7(9) required that he or his legal representative should be entitled to question other witnesses, determined by me, who have appeared before me.

3.24. Secondly, the audi alteram partem rule required that, as an implicated person, the President is entitled to the documents and records gathered in the course of the investigation, to enable him to prepare his evidence.

3.25. Thirdly, the Presidency required a full opportunity to be heard in order to avoid remedial actions – that would be binding on him – based on evidence not tested by the President as an implicated person.

3.26. After providing the written questions to the Presidency, he made somewhat of an about-turn by deciding that in fact before deposing to an affidavit, he still required a list of witnesses, statements, affidavits and transcripts of any oral testimony and wanted to question witnesses.

[1 Transcript of a meeting held between the Public Protector South Africa and President Zuma on 6 October 2016.]

3.27. The Presidency accordingly declined to provide answers to my written questions and cancelled the meeting for 10 October 2016.

3.28. The Presidency concluded by objecting to my statement at the 6 October 2016 meeting that I was in a hurry to complete the investigation, which was not ‘part heard’. The Presidency suggested that the investigation could just as well be completed after my term as the current Public Protector expired, as with other pending investigations. The President’s diary was determined well in advance and did not allow him to attend to the matter within the truncated period.

3.29. The Presidency requested an undertaking by the following day, 11 October 2016, that I would not conclude the investigation and issue any report until he had received the aforesaid.

3.30. On 11 October 2016 I wrote a letter to the President in response. I reassured him that I had, to date, not concluded my investigations into this matter and had made no adverse finding against the President.

3.31. I undertook that this office would comply with its duties under the Constitution, the Public Protector Act, Executive Members Ethics Act and all other relevant laws in conducting this investigation and submitting the report.

3.32. I noted that I had, since my first letter to him dated 22 March 2016, gone to great lengths to provide him with sufficient detail regarding evidence implicating him and the response required from him.

3.33. I had, in compliance with the Public Protector Act and the law on administrative justice, provided him with ample opportunity to respond in connection therewith.

3.34. The Notice in terms of section 7(9) of the Public Protector Act was merely one in a succession of letters to him canvassing substantially similar issues regarding this matter.

3.35. I noted my concern that he had, on two occasions, undertaken to provide a response to questions put to him in writing; when the time arose, he changed his mind and refused to provide responses.

3.36. I advised that it was incumbent upon him to provide responses within a period that I decide is both convenient and practical to me, given that firstly the Constitution requires him to assist and protect this office. Secondly the Constitution prohibited him from interfering with the functioning of this office. Thirdly, the Public Protector Act vests in me the discretion to require him to provide me with an expedited response. Finally, the spirit of the Constitution and the Public Protector Act requires him to cooperate fully in the investigation process; conversely, recalcitrant witnesses, particularly high-ranking members of the Executive such as him, should be regarded as violating both the letter and spirit of the Constitution and the Public Protector Act.

3.37. I advised that I had provided him with the evidence of the witnesses implicating him. He was not entitled to the full record of investigations as a condition precedent to answering the questions I had put to him.

3.38. I requested the questions he wished to pose to witnesses who had appeared before me. I undertook to make a determination on such questions in accordance with the Public Protector Act.

3.39. I advised that he was not entitled to refuse to answer the questions I had put to him prior to questioning other witnesses who had appeared before me. His right to question witnesses was not a sine qua non for his response to my questions.

3.40. I concluded by stating that it was in the President’s interests, and that of the people of South Africa, to account fully and honestly regarding the allegations against him.

3.41. I afforded the President a further extension to answer the questions put to him by no later than 11 am, Thursday, 13 October 2016 to enable this office to conclude the investigation and issue its report on the outcome thereof as soon as possible.

4. THE INVESTIGATION

4.1. Methodology

a) The investigation was conducted in terms of section 182 of the Constitution and sections 6 and 7 of the Public Protector Act.

b) Due to the fact that the second complaint by Honourable Mmusi Maimane was laid in terms of the Executive Members’ Ethics Act, 1998, I was compelled to conduct a formal investigation into the matter. The Act requires that The Public Protector must investigate any alleged breach of the code of ethics on receipt of a complaint. Section 3(2) of the Act further provides that the Public Protector must submit a report on the alleged breach of the code of ethics within 30 days of receipt of the complaint.

4.2. Approach to the investigation

a) Like every Public Protector investigation, the investigation was approached using an enquiry process that seeks to find out:

- What happened?

- What should have happened?

- Is there a discrepancy between what happened and what should have happened and does that deviation amount to maladministration?

- In the event of maladministration what would it take to remedy the wrongful acts.

b) The question regarding what happened is resolved through a factual enquiry relying on the evidence provided by the parties and independently sourced during the investigation. In this particular case, the factual enquiry principally focused on the following:

Alleged breach of Executive Members’ Ethics Act, 1998

c) Based on an analysis of the complaint, the following issues were identified as relevant for investigation:

a) Whether President Zuma improperly and in violation of the Executive Ethics Code, allowed members of the Gupta family and his son, to be involved in the process of removal and appointment of the Minister of Finance in December 2015;

b) Whether President Zuma improperly and in violation of the Executive Ethics Code, allowed members of the Gupta family and his son, to engage or be involved in the process of removal and appointing of various members of Cabinet;

c) Whether President Zuma improperly and in violation of the Executive Ethics Code, allowed members of the Gupta family and his son, to be involved in the process of appointing members of Board of Directors of SOEs;

d) Whether President Zuma has enabled or turned a blind eye, in violation of the Executive Ethics Code, to alleged corrupt practices by the Gupta family and his son in relation to allegedly linking appointments to quid pro quo conditions;

e) Whether President Zuma and other Cabinet members improperly interfered in the relationship between banks and Gupta owned companies thus giving preferential treatment to such companies on a matter that should have been handled by independent regulatory bodies;

f) Whether President Zuma improperly and in violation of the Executive Ethics Code exposed himself to any situation involving the risk of conflict between his official duties and his private interest or use his position or information entrusted to him to enrich himself and businesses owned by the Gupta family and his son to be given preferential treatment in the award of state contracts, business financing and trading licences; and

g) Whether anyone was prejudiced by the conduct of President Zuma.

Awarding of contracts by certain State owned entities to entities linked to the Gupta family

a) Whether any state functionary in any organ of state or other person acted unlawfully, improperly or corruptly in connection with the appointment or removal of Ministers and Boards of Directors of SOEs;

b) Whether any state functionary in any organ of state or other person acted unlawfully, improperly or corruptly in connection with the award of state contracts or tenders to Gupta linked companies or persons;

c) Whether any state functionary in any organ of state or other person acted unlawfully, improperly or corruptly in connection with the extension of state provided business financing facilities to Gupta linked companies or persons;

d) Whether any state functionary in any organ of state or other person acted unlawfully, improperly or corruptly in connection with exchange of gifts in relation to Gupta linked companies or persons; and

e) Whether any person/entity was prejudiced due to the conduct of the SOE.

d) The enquiry regarding what should have happened, focuses on the law or rules that regulate the standard that should have been met by the President and the implicated State Owned Entities to prevent maladministration and prejudice.

e) The enquiry regarding the remedy or remedial action seeks to explore options for redressing the consequences of maladministration.

4.3. At the onset of this investigation, I took the decision to review media articles which made allegations of undue influence being given to the Gupta family as well as Mr D. Zuma with regards to contracts awarded by SOEs.

4.4. I found the following SOEs were implicated in allegations of impropriety by the media:

a) Eskom SOC Limited (“Eskom”);

b) Transnet SOC Limited (“Transnet”);

c) Denel SOC Limited (“Denel”);

d) South African Airways (“SAA”); and

e) South African Broadcasting Corporation (“SABC”).

Allegations raised against Eskom

4.5. Eskom is South Africa’s main power utility. It uses a mix of nuclear, diesel, hydroelectric, pump storage, solar and coal to meet South Africa’s energy supply demand.

4.6. South Africa produces an average of 224 million tons of marketable coal annually, making it the fifth largest coal producing country in the world. Twenty-five percent (25%) of our production is exported internationally, making South Africa the third largest coal exporting country in the world. The remainder of South Africa's coal production feeds the various local industries, with fifty-three percent (53%) used for electricity generation. Coal has traditionally dominated the energy supply sector in South Africa. This domination is unlikely to change in the next decade, due to the relative lack of suitable alternatives to coal as an energy source.

4.7. The key role played by our coal reserves in the economy is illustrated by the fact that Eskom is the seventh (7th) largest electricity generator in the world. Eskom had thirteen (13) coal-fired power stations and maintained thirty-three (33) coal contracts serviced by at least twenty-eight (28) suppliers in December 2015.

4.8. I discuss below, the key allegations raised against Eskom in the media.

4.9. I noted an article in the City Press newspaper dated 12 June 2016 with the title “How Eskom bailed out the Guptas”. The key points of the media article are: