The PIC and GEPF – an update

18 April 2018

INTRODUCTION

Much has happened within South Africa, the PIC, and the GEPF (the Fund) since the HSF released its last briefs on these intertwined subjects. Most relevant to the topic at hand, the country has managed for the time-being to stave off junk status and the former tainted Deputy Minister of Finance Sfiso Buthelezi has been replaced by Mondli Gungubene – the latter therefore becomes the new PIC board chairman in place of Buthelezi.

Gungubene holds a B Com Law, was mayor of Ekurhuleni from 2010 until 2016 and was an outspoken Zuma critic. Journalists dubbed him ‘the lord of corporate governance’ because of his hardy questioning style during the Communications and Public Enterprise Committee Hearings. [1] While this change at the top is of course a very welcome, the risks and challenges facing the PIC, GEPF and its members have not yet begun to subside. If anything, they have crystallized.

ESKOM

The difficult situation in which the GEPF finds itself follow from the PIC’s R95bn investment in Eskom came to fruition in February this year when the PIC was forced to extend a R5bn one month loan to the parastatal. In a letter sent by the PIC CEO Dan Matjila to Parliament’s standing committee on finance, Matjila revealed that without the PIC’s R5bn loan, Eskom’s going-concern status would have been jeopardised and that the PIC’s R95bn government-guaranteed exposure was at serious risk. [2]

This makes clear the massive risk that has resulted from the PIC being Eskom’s lender of last resort since 2014 when the PIC began buying Eskom debt in private placements after demand from other buyers dried up. Through the PIC, the GEPF’s Eskom long term bond holdings increased from R74bn in 2016 to R84bn in 2017 alone. So while Eskom’s Board and Executive team have finally been replaced, it would not only prudent but necessary to highlight the challenges Eskom faces in order to protect GEPF investments and hold the new leadership to account.

The following is taken from a presentation by Anton van Dalsen – legal counsel to the HSF – in response to Eskom’s 2018 RCA Applications: Eskom’s attitude towards revenue generation and cost management in the past can effectively be summarised as “we are selling less than forecast, but our expenses continue to rise and it is unfortunately the consumer’s duty to fill the gap.” Furthermore, Eskom’s problem has not been confined to cashflow management as there is a much more important issue at stake in that Eskom has an out-of-date business model. Briefly put, Eskom is faced by a combination of the following:

- an overly aggressive capital expenditure programme, coupled with an inability to avoid major cost overruns and multi-year delays;

- surplus generating capacity, which increases each year, not to mention the upcoming completion of the Medupi and Kusile power stations (idle capacity of this kind has obvious cost implications);

- the insertion of an IPP (renewable) programme by Government which Eskom has to pay for and has grown to dislike, since it would rather find customers for its own surplus electricity capacity;

- renewable energy which has by now become much cheaper than the alternatives - and instead of taking a longer term view and studying how renewables can be integrated in an efficient way, Eskom prefers a dismissive attitude;

- a fixation on “base load” energy, used as a justification for a nuclear energy programme which even if it were suitable for “base load” generation, is clearly unaffordable;

- a massive increase in borrowing (to finance capital expenditure), together with an interest bill which is certainly higher than originally foreseen, due to Eskom’s repeated credit downgrades;

- the slackening of demand as a result of limited economic growth; and

- consumer behaviour, which is not only trying to limit electricity usage, but is moving away from Eskom altogether, as a result of unpredictable supply over the past few years, expected further out-of-the-ordinary tariff increases and easily installed alternative energy sources, such as solar panels.

THE GEPF’S IRRECONCILABLE REASSURANCE TO MEMBERS AND PENSIONERS

According to Government Employee Pension Law, a member or pensioner has the right to communicate directly with the GEPF regards any matter that affects him or her personally. Therefore, given the concerns expressed by pensioners, members and others to the HSF around the risks facing the GEPF, and ultimately the security of the pensioner’s payouts, we urged pensioners to indeed contact the GEPF directly.

But when these and other pensioners approached the Fund and its Trustees with their concerns, no matter how detailed their questions, they were consistently stonewalled with generalised answers. The overriding response from the GEPF has been that members and pensioners need not worry because the pension fund is a defined benefit plan, and as such their pension payments are guaranteed by the employer i.e. the government. So should the Fund become underfunded, the government would step in to fill in the gap.

And this is where the paradox lies. If the Fund were to become underfunded, it could well be from defaults on its massive SOE debt holdings – around R165bn according to the latest annual report. So not only will the government be liable to bring the Fund back to fully-funded status in order to provide pension payouts, it will at the same time be burdened with failing parastatals. Whether Treasury will be able to manage both is a legitimate concern, and the PIC as well as the GEPF would do well to make up for their shortcomings in accountability and transparency that have become evident in the last few years.

TRANSPARENCY AND ACCOUNTABILITY

The major issues around transparency and accountability at the PIC and GEPF were discussed in two HSF briefs published in July and August last year entitled The Public Investment Corporation and The Government Employees Pension Fund – An Overview and Addressing the Concerns of Government Employee Pension Fund Members and Pensioners. Here we will sum up developments since then.

In response to the PIC’s R5bn one month loan to Eskom in February, there was major concern expressed by numerous GEPF stakeholders, most notably the Public Servants Association (PSA). When asked about these concerns, Matjila said the “The PIC is accountable to the GEPF directly in terms of the investment mandate signed between the two organisations.

The PIC is under no obligation to consult or inform any trade union when it implements the mandate of the GEPF.” [3] Subsequently however, according to PSA deputy GM Tahir Maepa, Matjila told the PSA that the PIC was under the impression the GEPF had discussed the issue with the union. Deon Botha as head of corporate affairs for the PIC followed this up with "The PIC apologised to the PSA and committed to improving communication with all stakeholders and clients in future, together with GEPF." [4]

These occurrences should come as a surprise given that one of the GEPF board’s strategic objectives for the 2017/18 financial year is to improve stakeholder relations. This does not bode well for the other strategic objectives aimed at addressing pitfalls within the GEPF in urgent need of attention, namely improving investment monitoring, better risk management and to make the financial statements more transparent. [5]

In an attempt to strengthen good governance at the PIC, the Democratic Alliance, with the backing of Cosatu and other trade unions, submitted a Private Members Bill to parliament in January this year. The Bill proposes six amendments to the Public Investment Corporation Act, most notably:

Instead of being appointed unilaterally by the Minister of Finance, the chairperson of the PIC is to be appointed by the Minister on the recommendation of the National Assembly and must have the necessary expertise, qualifications and good character as required by the Financial Advisory and Intermediary Services Act;

The Board of the PIC is to include a representative of registered trade unions whose members form the majority of the members of the GEPF.

This Bill also calls for an annual report reflecting all investments, whether listed or unlisted.

We submit however that a simple list does not provide the details required to hold the PIC as well as GEPF to account. For example, while GEPF does list its investments in this manner it has still not provided enough information on investments such as the controversial multibillion rand loan made to Iqbal Surve’s Independent Media as far back as 2013. And despite this investment having made no returns since, in March this year the PIC made a further R4.3bn investment into Ayo Technology Solutions, a subsidiary of the Sekunjalo Group also headed by Surve. [6]

Along the same vein, the PIC too refuses to provide details on the R9.3bn it provided to Lancaster 101 in 2016 as the BEE partner at Steinhoff International. This on top of the R25bn exposure the PIC already had to Steinhoff before the share price capitulated. [7] These unfortunately are only a few of many failed attempts to gain clarity within the GEPF’s R86bn portfolio of unlisted equities and direct loans investments.

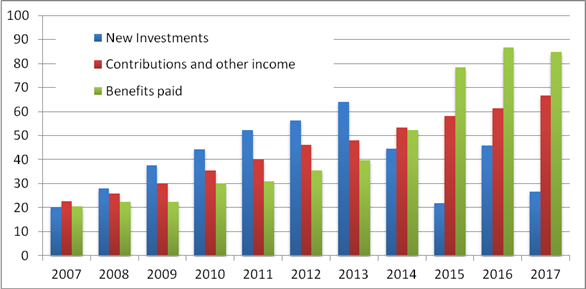

WORRYING GEPF FINANCIAL INDICATORS

Over the last four financial years and for the first time in the Fund’s history, three of the Fund’s important financial indicators have decoupled; cashflow out of the Fund in the form of benefits paid has exceeded cash inflows from contributions, and new investments made have decreased. [8]

[9]

[9]

Within the Fund’s 2017 Annual Report it was noted that “[T]he fund was making contributions at rates lower than recommended by the [Fund] actuaries” and “The shortfall has an impact in the funding level of the Fund.” And while the actuaries did conclude that the Fund currently stands at a minimum funding level of 121.5%, the long-term funding level was at 79.3%, which is below the 100% target.

Regards the drop in new investments, nowhere with the 2014/15 or 2016/17 reports was an explanation given. While there may well be legitimate reasons for this, such as a possible lack of investment opportunity, it does beg the question whether this will translate into a decrease in investment returns that’ll apply greater pressure to the funded status of the Fund.

CONCLUSION

There are hefty challenges that remain within the PIC and GEPF despite the new leadership at the helm of the former. Firstly, given that the PIC and GEPF are the largest investors in many of the SOEs, including Eskom, it is expected that the PIC should apply pressure on the parastatals regards governance and strategy, which in fact it should have been doing years ago.

Secondly, both the PIC and GEPF have major room for improvement regards transparency in the investment portfolios as well as improvements in stakeholder communications. Lastly and all importantly, these factors feed into the GEPF’s funded status and the security of pensions, with warning signs in the financial indicators of the last four financial years highlighting a need to greater responsibility and vigilance from the Board.

By Charles Collocott, Researcher, HSF, 18 April 2018

NOTES

[1] https://www.news24.com/SouthAfrica/News/i-choose-my-name-20170708

[5] https://www.moneyweb.co.za/in-depth/investigations/gep-saddled-with-dud-investments-and-worse/

[8] GEPF Monitoring Group, GEPF Cash Flow Analysis: 2008 to 2017.