IMF Executive Board Concludes 2013 Article IV Consultation with South Africa

October 1, 2013

On July 31, 2013 the Executive Board of the International Monetary Fund (IMF) concluded the Article IV consultation with South Africa (see here - PDF).

South Africa's economy has made important strides over the past two decades. Rising income levels have resulted in declining poverty rates, and strong institutions and policy frameworks have contributed to macroeconomic stability and greater integration with the global economy. However, in recent years the country's structural problems that are holding back growth and job creation have come to the fore.

The economy has underperformed other emerging markets and commodity exporters, exacerbating South Africa's already-high levels of unemployment (25 percent) and inequality, and contributing to rising social tensions. At the same time, weak trading partner growth, coupled with declining competitiveness and countercyclical fiscal policy, have led to rising fiscal and current account deficits and made South Africa vulnerable to a prolonged reversal of capital inflows and a further repricing of risk premia.

The rand has been one of the worst performing emerging market currencies in 2013, and bond yields rose sharply in May and June as concerns over the Fed's tapering of quantitative easing and China's growth outlook led to rising global risk aversion and weaker commodity prices.

The outlook is for continued sluggish growth and elevated current account deficits. Growth is projected at 2 percent in 2013 as weak consumption growth and lackluster private investment offset robust public investment and higher export growth. Growth is expected to rise to about 3 percent in 2014 and 3½ percent in the medium term, as infrastructure investment gradually relieves supply bottlenecks. Unemployment is expected to remain high.

A gradual withdrawal of stimulus is projected to result in declining fiscal deficits, but continued high imports for infrastructure investment will likely keep the current account deficit close to 6 percent of GDP throughout the projection period. Quicker implementation of much-needed structural reforms could result in higher growth and job creation.

The balance of risks is tilted firmly to the downside. The main risk is a prolonged stop in capital inflows and a disorderly adjustment in the twin deficits. The trigger could be either external, e.g., a global repricing of risk resulting from an unwinding of unconventional monetary policies in advanced economies, or a further escalation in domestic labor and social unrest. South Africa also remains vulnerable to a further weakening of growth in Europe or a slowdown in China and other emerging markets, particularly if accompanied by a weakening of commodity prices.

Executive Board Assessment

Executive Directors commended the significant macroeconomic progress made by South Africa over the past two decades. However, Directors noted that lower growth in recent years, due to external and domestic factors, has aggravated already high unemployment and inequality. In addition, large current account and fiscal deficits have increased. To address the vulnerabilities, create jobs, and foster inclusive growth, Directors stressed the need for firm policy action and progress on reforms.

Directors welcomed the authorities' National Development Plan, which outlines an integrated strategy for structural reforms. They emphasized the importance of decisive and timely implementation of this plan. Directors underscored that additional labor and product markets reforms, improvements in the business climate, and trade liberalization will also be critical to achieve faster growth and job creation.

Directors agreed with the need for gradual fiscal consolidation and welcomed the authorities' commitment to remain within the medium-term expenditure ceilings. If growth continues to disappoint, they saw merit in allowing automatic stabilizers to operate this year, provided financing conditions permit. Directors underscored the need to stabilize debt and rebuild fiscal buffers, and generally agreed that announcing a debt target could help bolster the credibility of the medium-term fiscal outlook. They commended the authorities' commitment to long-term fiscal discipline and welcomed ongoing reforms to improve spending efficiency.

Directors agreed that the monetary policy stance is finely balanced and the inflation targeting framework remains appropriate. They concurred that the exchange rate pass-through to inflation and wage settlements are critical factors in determining the next monetary policy move. Directors encouraged the authorities to stand ready to adjust interest rates as needed.

Directors observed that South Africa's highly flexible exchange rate is a considerable strength and should be maintained. Noting the costs of accumulating and managing foreign exchange reserves, Directors in general agreed that increasing reserves will further contribute to lower vulnerabilities. They encouraged the authorities to give consideration to regular and pre-announced auctions to buy foreign exchange as done by some other countries. Directors also encouraged the authorities to promote foreign direct investment and considered that structural reforms are also needed to raise the low household savings rate and improve the external position, which is assessed to be weaker than justified by fundamentals.

Directors noted that South Africa's financial system is well capitalized, but risks from unsecured lending have risen. They welcomed the authorities' ongoing efforts to improve the regulatory and supervisory architecture, including the recent adoption of Basel III standards. Directors noted that the rapid expansion of unsecured credit from a low base has contributed to financial inclusion, but highlighted areas where new measures could play a useful role to bolster financial stability and help households deal with high indebtedness. They emphasized that heightened vigilance is important to ensure that these risks do not become systemic and encouraged increased coordination among regulators.

Issued by the IMF, October 1 2013 (the full statement including tables can be accessed here)

Extract from the report:

Fiscal position

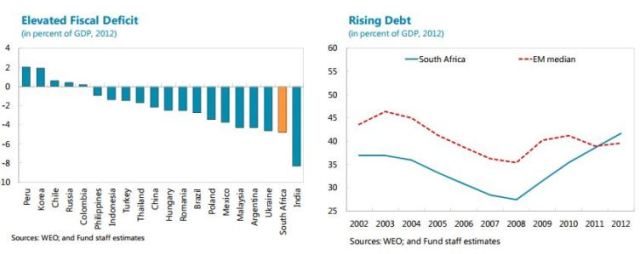

13. South Africa's relative fiscal position among EMs has weakened.

General government deficits have averaged 5 percent of GDP for the past four years as South Africa took advantage of the fiscal space that existed pre-2008 to support the economy. As a result, government debt increased by 15 percentage points to 42 percent of GDP, slightly above the median in EM peers (Figure 5).

A cyclical decline in revenues has played a role, but most of the deficit deterioration since 2007/08 is due to a near-doubling of the wage bill which now absorbs more than 35 percent of spending, compared to an average 22 percent among EM peers. This reduces expenditure flexibility and crowds out government capital spending which is increasingly undertaken by public enterprises. Public enterprise borrowing has more than quadrupled to 14 percent of GDP since 2007/08, raising contingent liabilities.

Last year's agreement to limit public sector real wage increases for the next three years to 1 percent and this year's decision to set explicit expenditure ceilings should facilitate the planned withdrawal of fiscal stimulus. However, the government's poor record in controlling the wage bill and potential spillovers from high wage demands in other sectors represent downside risks. Moreover, at 2.7 percent of GDP in 2012/13, the national government primary deficit falls short of the 1.9 percent of GDP necessary to stabilize the debt under prevailing low interest rates, suggesting debt would rise quickly should the envisaged consolidation fail to materialize or interest rates rise faster than projected. [The debt-stabilizing primary balance is estimated to increase to -0.6 percent of GDP in the medium term as global interest rates normalize.]

Rising deficits have more than doubled the government's gross financing need compared to 2008, which at 12 percent of GDP is above the EM average notwithstanding an average debt tenor of 11 years. Nearly 60 percent of the 2012/13 borrowing requirement was financed by nonresidents, which had led to a substantial yield compression before the recent sell-off.

Financial stability

14. Financial soundness indicators remain strong, but the rapid expansion of unsecured lending to households has increased credit risk. Bank capital is well-above the regulatory minimum and profitability remains strong (Figure 6). But unsecured credit to households, mainly personal loans, has more than doubled over the past three years, now accounting for about 12 percent of banks' total credit exposure, which combined with their large mortgage portfolio, brings banks' exposure to highly leveraged households to 60 percent (Box 2).

Tighter lending standards and reduced profitability on mortgages, the promulgation of the 2007 Credit Act, combined with the objective to promote financial inclusion, led to a sharp rise in unsecured lending. While the increase in unsecured credit to low-income households from 1.6 to 2.2 percent of disposable income since 2008 has contributed to greater financial inclusion, there is still a need to improve access to finance, especially for SMEs, according to the World Bank.7 Rising credit has worsened household debt burdens, which now amounts to 76 percent of disposable income, and has added to social vulnerabilities.

Higher interest rates, weaker household incomes growth, or lower house prices could pressure households' debt repayments, nonperforming loans (NPLs), and banks' capital given relatively low provisioning in international comparisons. Banks' reliance on short-term wholesale funding provided mostly by residents also represents a vulnerability, though historically it has been stable as it corresponds to corporate deposits and contractual savings in pensions and insurance funds that are subject to capital controls. In addition, South African banking groups' expansion on the African continent would require additional efforts to improve home-host cooperation among regulatory authorities.

The full report can be accessed here - PDF

Click here to sign up to receive our free daily headline email newsletter