Lockdown: Consequences to linger many years

27 August 2020

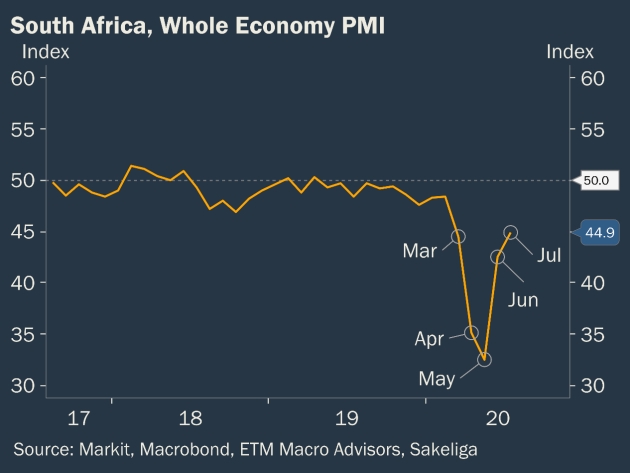

Extremely challenging business conditions, smaller markets, mass retrenchments and reduced incomes were evident over the period of the lockdown even up to August 2020. Many economic indicators now reveal the severe impact of the draconian Covid-19 lockdown with its many irrational and unjustified impediments to economic value creation. This is according to the business group Sakeliga’s Economic Update for Business Decision-making for August 2020, a quarterly report released in collaboration with ETM Macro Advisors today.

The report points to a severe impact of the Covid-19 lockdown. Businesses are advised in the report to prepare for a smaller economy and 10-20% smaller turnover and earnings over the medium-term compared to pre-lockdown levels. Other indices in the report revealed plummeting industrial production as well as deep declines in tax income.

Furthermore, indications are also emerging that firms initially spared the adverse effects of lockdown are now starting to experience harsher operating conditions.

“Clearly, a 10-20% reduction in turnover and earnings will not only affect hiring, but also business expansion plans, new investment, as well as the ability of the private sector to make the most of any upswing in commodity markets,” says Gerhard van Onselen, Senior Analyst at Sakeliga.

“The adverse effects of the lockdown are likely to linger for a significant time to come. Not only have jobs been lost and incomes and savings been reduced– with likely increases in debt across the board – but irrational and incoherent restrictions remain in various sectors. Asides from the remaining restrictions and problems with electricity supply, threats of new taxes on all levels of government will likely only increase as the state becomes more and more desperate for resources.”

The report points to the possibility of a government borrowing requirement expanding to R1 trillion, much larger than National Treasury’s forecasts of R770 billion presented in the supplementary budget.

“To make matters worse”, Van Onselen adds, “continued threats about a return to stringent hard lockdown measures are made on a nearly daily basis by public officials, seemingly with little concern over the harms to livelihoods. It is certainly only logical to expect firms to be vigilant with investments and expansions under such uncertainty about the state’s policies and regulations. Such policy uncertainty, however, obstructs economic recovery. Less obstructive forms of risk mitigation should be considered.”

Presidential policy scorecard

The report also provides a presidential policy scorecard for South Africa. This scorecard is intended to track the real impact of the current administration’s actual economic policies expressed by several factors such as investment measures, currency, bond yields, energy production, political constraints on industry and fiscal stress.

The business cycle adjusted Sakeliga-ETM presidential policy scorecard gives the Ramaphosa administration a current score of 20 out of 100. It is urgent that this score rises at least above 40 to stem some of the tremendous loss of confidence in the aftermath of the stringent and irrational Covid-19 lockdown.

In order to improve its score, says Van Onselen, the current administration would have to not only end remaining lockdown regulations and replace those with voluntary health recommendations if need be, but should also review many other policies that hamper value creation. Such policies include labour regulation, BEE, taxes and state expenditure.

“In the aftermath of lockdown, the time has arrived for more business and less politics. Centralised political risk management and one-sided interventions and prohibitions have been employed with predictably disastrous consequences. Government should now urgently review its policies and allow freedom for economic recovery to happen," Van Onselen concludes.

Issued by Gerhard van Onselen, Senior Analyst, 27 August 2020